How Life Insurance Provides Financial Security for Your Family After You're Gone

There are several different types of insurance coverages you will be recommended to have throughout your lifetime. For example, car insurance in the case of theft or coverage for you and the other driver if you are involved in a car accident. House insurance in the case of a fire or burglary. Health insurance in the case of a medical emergency. However, of all the possible insurance coverages, one of the most essential is life insurance because it protects and prevents immediate financial hardship for your loved ones after you have passed away.

Life insurance is a contract between you, the policyholder, and an insurance company. When you decide to get life insurance, you will decide on the coverage amount. (You can increase or decrease your initial coverage amount throughout the life of the policy). For example, you may choose to get an insurance policy with a coverage of $50,000. As a result, after your death, the life insurance company will pay out $50,000 to the beneficiary of your policy. The beneficiary is the person(s) of your choice, which could be your spouse, child(ren), parent(s), or someone else.

The financial security of life insurance

Life insurance is important because it ensures your family will receive a financial payout that, pending the amount, will cover your burial and provide financial security well after your death.

After the burial, other expenses that the payment from the life insurance could help cover include the following:

- Everyday expenses: monthly bills, groceries, and other essentials

- Outstanding debts: mortgages, credit card debt, and student loans

- Child or dependent care: help fund programs such as daycare

- College cost: help give money to kids so they can go to college

The cost of life insurance

A common mishap with insurance coverage is either people choosing not to get coverage or allowing their coverage to lapse by no longer paying the monthly premium. If you stop paying, your policy is no longer active, and the insurance company will not pay.

On average, the rate of life insurance is $26 per month. Although life insurance is relatively inexpensive, it is one of the first expenses people let go of if they fall upon financial hardship.

Recommended: A life insurance calculator can help determine the different rates.

Most insurance companies offer a "grace period" to pay money owed if you miss a payment. However, if you do not pay the money owed by the end of the grace period, you are subject to having your life insurance policy ended.

A financial hack for life insurance is to pay in advance for a set period of time, such as six months of coverage or one year of coverage. By paying in advance, the premium will usually be at a discount. For example, if you pay monthly, your fee may be $20 per month. However, if you pay for one year, your payment may only be $90, saving you $30 had you paid monthly for one year.

How to choose the right policy plan

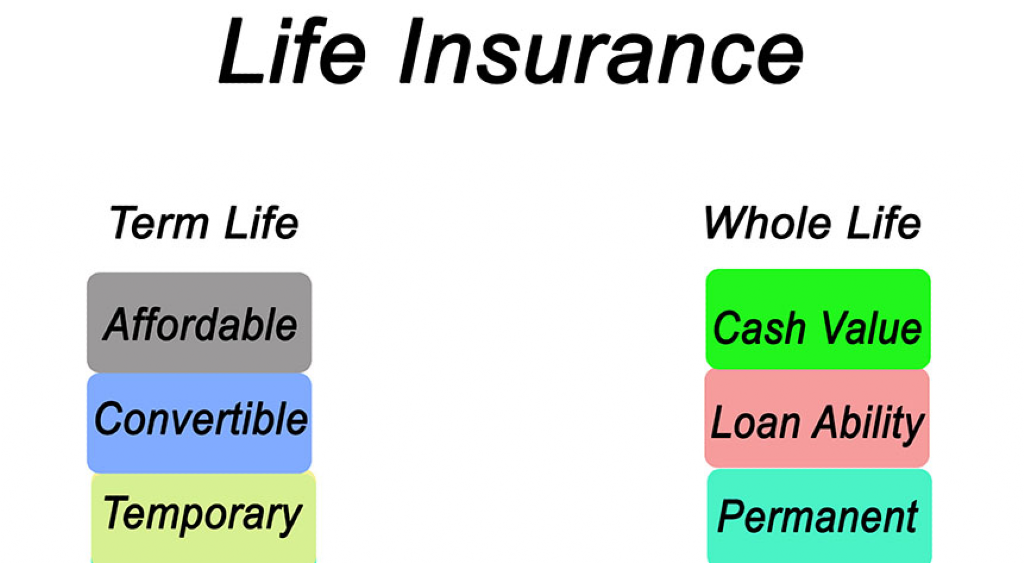

When choosing a plan, it is crucial to think about how long you wish for the premium to last. There are two common types of life insurance: term and permanent.

Term life is the cheaper option of the two, but it has an expiration date. The policy could range from 10 to 30 years, depending on your choice of the policy's duration. If you choose term life, it is important to always keep up with the expiration date of your policy. For example, suppose the time has expired without the policyholder's knowledge. In that case, unfortunately, your family will think they have an insurance policy to help with expenses that after your death, only to be informed that the policy has expired.

A permanent life insurance plan is intact until your death. Though this type of insurance may seem more beneficial to ensure your family is financially comfortable, it is also more expensive than a term life insurance plan. According to State Farm, a 35-year-old woman in peak physical condition wishing to purchase a $500,000 term life insurance policy would have to pay $36 per month for a 30-year plan. On the other hand, if the woman wanted to purchase permanent life insurance, it would cost her around $480 per month until she passes away.

Whether term or permanent life insurance, many people often confuse life insurance with burial insurance. Burial insurance is usually $50,000 or less, and the money is mainly used to cover burial expenses. On the other hand, life insurance can be millions of dollars in coverage and can be used for long-term financial security for your family.

In conclusion, regardless of the type of life insurance purchased, the coverage will help bring peace of mind to you and your family by knowing at death, even though there may be sadness, there is protection from extreme financial hardships.