What is Afterpay? How Does Buy Now, Pay Later Work?

- Afterpay is a buy now, pay later service, which allows customers to purchase items and pay in installments.

- Buy now, pay later typically allows customers to pay 25% upfront, and the remaining balance in a series of 3-4 payment options.

- There are many pros and cons of using Afterpay; one con is that many users end up in debt after using the service.

Afterpay is a buy now pay later (BNPL) service that breaks your payments into installments. This way, the customer isn’t spending so much at one time but instead spreading the cost over time. Afterpay accounts and similar buy now pay later apps have been increasing in popularity. However, many users don’t quite understand how Afterpay works, yet sign up for it anyway.

What is Afterpay?

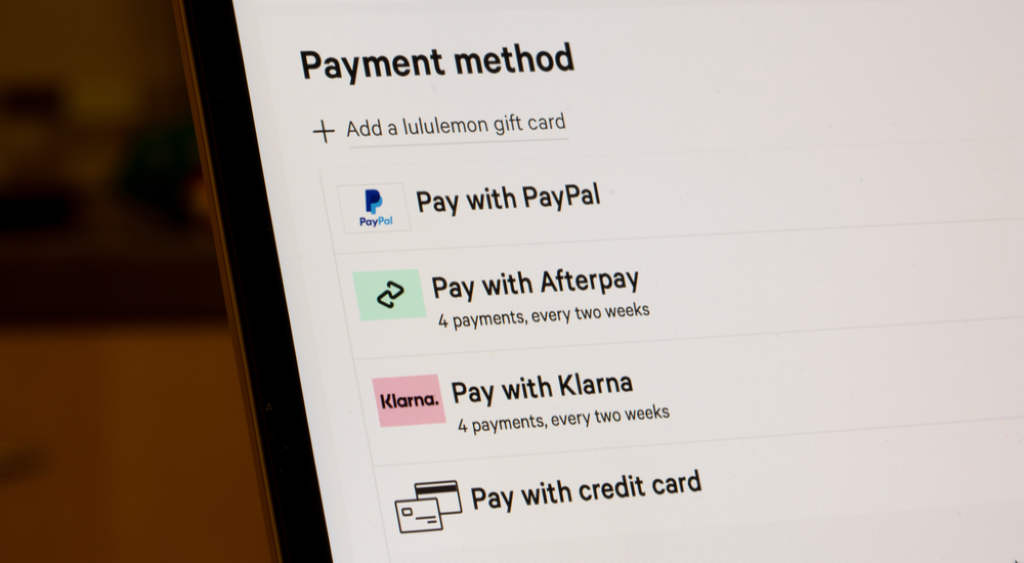

Afterpay or other BNPL apps give customers the option to purchase items and then pay in installments. At checkout, the customer is typically given the choice of paying a percentage upfront and billed for the remaining amount in 3-4 payments at a later date. For example, with pay-in-four installments, the customer will pay 25% upfront and typically another 25% every two weeks until the balance is paid off. Some BNPL apps even allow customers to pay $0 upfront and finance the remaining amount later.

Image Credit: Tada Images / Shutterstock.com

As buy now, pay later services are becoming more popular, customers see these options as they checkout when shopping online and sometimes when shopping in person. Customers can then choose the Afterpay option at online checkout and pay $0 or a portion of their total with a debit or credit card.

How Does it Work?

Buy now, pay later apps, including the Afterpay app, work by splitting your purchases into smaller payments. By definition, these apps will loan you money without charging interest or fees as long as users make their payments on time. Customers who miss payments are billed interest, late fees, or both.

The BNPL apps charge a fee to the retailer to earn money, and any applicable late fees or interest on loans from users are also a revenue stream. However, some BNPL apps do not charge interest, depending on your credit score.

Affirm, another BNPL company, requires a soft credit check when customers sign up for an account. However, Affirm may perform a hard credit inquiry to give the customer accurate payment options based on their credit when making a purchase. Though soft credit checks aren’t recorded on your credit report, hard inquiries are. If you plan to rebuild or increase your credit score, this is something to consider, as a hard inquiry can negatively affect your credit.

Image Credit: Shutterstock.com

Regarding late fees, Affirm will let you reschedule your payment to avoid any fees. Although Affirm’s official policy will not charge users late fees, if your minimum payment is late or not paid in full, your late activity could be reported to the credit bureaus. Therefore, these late payments could negatively affect your credit score and increase any future interest rates offered to you.

On the other hand, Afterpay does not perform any credit checks. Instead, Afterpay monitors your payments, and you may be charged a $10 fee if you are late. Another $7 fee is applied if your account does not become current after seven days.

The Pros and Cons of Afterpay and Other BNPL Apps

According to an article by The Hustle, 75% of BNPL users in the United States are either millennials or Gen Z. Some speculate that these generations are more likely to use these types of financing options due to their fear of credit card debt.

BNPL companies claim that their services are superior to overusing credit cards because users can spread their payments over a period of time, making purchases more affordable. Users can also get cut off if they miss multiple payments. In addition, some apps won’t let users roll over their balance, which prevents them from racking up more debt.

Image Credit: Tada Images / Shutterstock.com

However, many users are still ending up in debt. According to the Hustle, 15% of Australian BNPL users had to take out loans to pay off purchases. In the UK, one bank reported that 10% of BNPL users overdrew their bank accounts in the same month.

The Money Wrap-Up

Despite the risks of landing in debt, merchants and users alike are increasingly using BNPL services. In fact, according to The Hustle, merchants who use Afterpay will see a 17% increase in shopping cart volume and a 12% boost in sales. However, regardless of how convenient it is to use these services, it is important to fully understand what you’re signing up for before you agree to use any BNPL service.

Main Image Credit: Tada Images / Shutterstock.com