Tips on How To Improve Your Credit Score

- Your credit score indicates to credit bureaus and financial institutions how trustworthy you are with money.

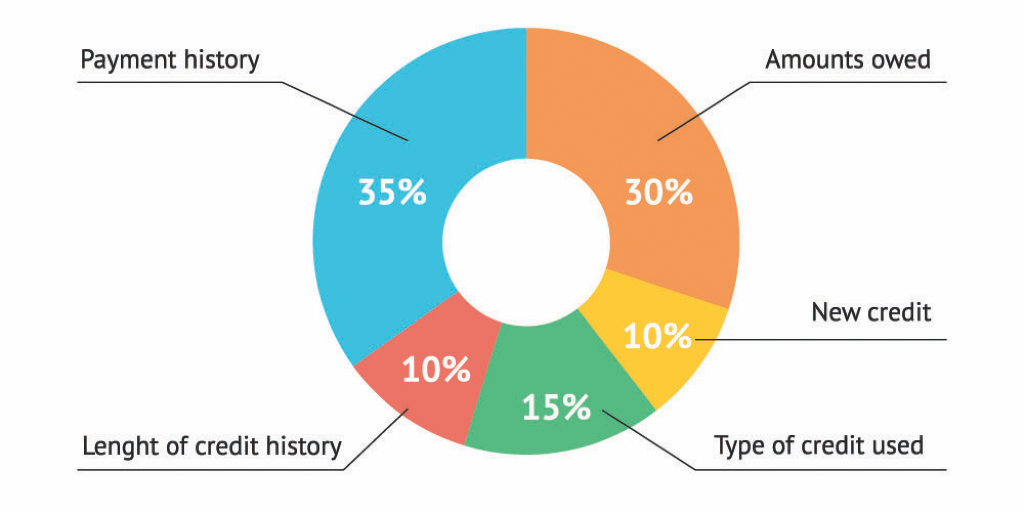

- The following five factors make up your credit score: (1) payment history, (2) amount of money owed, (3) credit history, (4) different types of credit owned, and (5) applying for new credit.

- You should not get discouraged if you have a low credit score because there is always room for improvement.

When applying for a loan to make large financial purchases, such as a home or a car, one of the things the lender takes a look at is your credit score. Your credit score is important because it is part of the decision to either approve or deny your loan request when you apply to receive loans from financial institutions. Financial institutions do not give out money to anyone. Your credit score equates to your creditworthiness, which can also be described as how much the bank can trust that over time they will receive their money back from you as a borrower.

Lenders may request any credit reports from credit reporting agencies in order to look at your credit score and check your credibility and responsibility with regard to money. It is important to have a good credit score to maximize your chances of securing a loan. If you are looking to improve your score, below are some helpful tips that can help you increase your score, starting today.

What is a Credit Score?

A credit score is a number that tells creditors how trustworthy you are with other people’s money and if you can pay it back on time. When applying for a loan or setting up a payment plan, creditors will use your credit score to determine what repayment plan to give you. The better your credit score, the lower the interest rate on your payment plan.

Credit scores range from 300-850, and the higher, the better. Sometimes lenders use a brand or type of credit score, such as a FICO score. FICO scores are one of the most common types of credit scores and are calculated by taking the credit scores from the top credit reporting agencies. When your credit score is being calculated, there are five factors that can affect your score.

Payment History

This factor determines how responsible you are as a borrower with your payments. If you have made timely payments consistently, your credit score will be impacted positively. On the other hand, if you have missed multiple payments, your credit score will be impacted negatively. This factor accounts for 35% of your credit score.

Amount of Money Owed

Another factor that counts up for a large amount of your credit score is the amount of money you owe at the end of the month, compared to your revolving credit. It is important to note that when using your credit card, it is recommended not to use over 30% of your allowed credit limit. Using over the 30% threshold can be a red flag to creditors, which in turn, negatively impacts your credit score. By keeping your credit utilization ratio under 30%, your credit score will be impacted positively. This factor accounts for 30% of your credit score.

Credit History

Creditors also look at your credit history. Typically, when someone has a longer credit history, their credit score will be impacted positively, leading to the creditors giving them loans with lower interest rates.

If you recently got your first loan or credit card, your credit history may be short. Continue paying your bills on time and keeping your credit utilization rate low. Paying expenses off on time will help establish your credit history and your reputation as a responsible spender.

Another way to update your credit history, in a relatively quick time frame, is to have a trusted guardian or parent with established credit history add you as an authorized user to one of their longer established credit lines, such as a credit card that has been opened for 7+ years. By adding you as an authorized user, the trusted parent or guardian will be able to transfer the positive impact of their credit history with you, which may boost your credit score. It is important to note that if the guardian or parent does not have excellent credit or credit history, this may impact your credit score negatively.

Overall, credit history makes up 15% of your credit score.

Different Types of Credit

The fourth factor that makes up your credit score is the credit mix. The typical types of credit accounts consist of student loans, auto loans, a mortgage, and credit cards. Those who have a larger variety of credit accounts, as long as they are adequately managed, the more likely your credit score will be positively impacted. This section accounts for 10% of your credit score.

Applying for New Credit

Applying for new credit may negatively affect your credit score if you are applying too frequently. The frequency could imply that you are having difficulty paying off your current bills. Thus, you are using new credit to pay off old credit, which is a vicious cycle and something that you should avoid.

This section also accounts for 10% of your credit score.

Tips to Increase or Build Your Credit Score

Tip #1: Avoid late payments; pay your bills on time

It is important to avoid late payments because they are reported by lenders and stay on your credit report for seven years. In addition, when using someone else’s money to purchase items, it is crucial to pay them back on time to ensure your reputation and credibility do not get damaged.

When buying things using your credit card, keep your receipts, keep track of your purchases, and payment due dates. Keeping track of your activity will help you stay organized and make payments on time. Furthermore, it will help you comprehend your spending habits and how much money you need to pay back to your lenders. By avoiding late payments and paying your bills on time, you will be raising your credit score considerably.

Tip #2: Do not max out your credit card.

Another thing credit bureaus look at when considering giving you credit is the percentage of your credit card limit being used. As mentioned above, the general rule of thumb is not to spend more than 30% of your credit limit.

Tip #3: Do not apply to too many credit cards at the same time.

Applying for multiple credit cards simultaneously sets off a red flag. It leads them to assume you are having trouble paying your bills, leading to you having to ask for more money to pay off your current expenses. Of course, if you wish to own multiple credit cards, that is fine. However, make sure that when applying for them, the application processes are spaced out accordingly.

Tip #4: Use your credit card wisely.

Nearly half of the United States population has credit card debt. Credit cards may be beneficial when you need to secure a loan from a financial institution. However, if you misuse credit cards, it will have negative repercussions, such as higher interest rates and a poor credit score.

To ensure that you are not spending more than you can afford, always make an effort to keep track of your expenses and credit card balances.

Checking your credit score often will allow you to see where you stand as a borrower. Your credit score is one of your most important assets; therefore, it is important to ensure that your score does not drop too low.

Using the tips mentioned above, you can maintain, build, or improve your credit score and receive the best rates when applying for credit or loans.

Sources: Experian