How is Crypto Taxed?

- As the crypto market is relatively new and rapidly evolving, many were able to profit from this industry without any tax due.

- The Internal Revenue Service (IRS) has decided to begin taxing cryptocurrency profits as many did not report having crypto assets, leading to them understating their income and the amount of taxes paid.

- It is essential to know what crypto activities the IRS views as taxable, so the taxable income at the end of the year is neither overstated nor understated.

Cryptocurrency has become increasingly popular in today’s society and has led to many profiting off of their investments. However, due to people's significant gains via this revolutionary market, the Internal Revenue Service (IRS) has become concerned about the taxable income many are reporting on their tax returns.

Why Cryptocurrency is Getting Taxed

As the trading of digital currencies has begun to increase over the past couple of years exponentially, this has led to the IRS stating relevant cryptocurrency transactions must be disclosed as taxable income.

The IRS’s reasoning regarding taxing crypto and making them subject to taxes is that many were not reporting their gains in the past, which led them to make a large sum of money without paying federal income taxes.

What is Viewed as Cryptocurrency by the IRS

Due to the continuing advances in the cryptocurrency space, it is difficult to determine what the IRS views as taxable crypto income. Consider discussing your filing status and tax information with a trusted tax preparer if you are unsure. Below are some examples of cryptocurrency transactions the IRS views as taxable or non-taxable.

Taxable

Selling Crypto

When selling crypto, the transaction price usually differs from the purchase price. Consequently, the digital asset's value change can become taxable income if the selling price exceeds the purchase price. However, if it is a loss, it can be claimed as a loss during the tax return process, resulting in a standard deduction in the net amount of taxes to be paid.

Receiving Crypto for a Service

Receiving crypto from someone performing a service is also another form of taxable income. When the crypto is accepted, it is viewed as a digital asset as compensation for work. Consequently, it is considered income, and its assigned value is the market value when the asset switches hands.

Trading Crypto

Trading crypto is another taxable income as typically, the digital assets are held for short periods before being exchanged to acquire another form of crypto.

Image Credit: Shutterstock.com

Non-Taxable

Donations to Charitable Organizations

If crypto is donated to a charitable organization, the donated amount cannot be taxed by the IRS. The criteria that a charitable organization must meet so the IRS does not tax donations can be viewed here.

Purchasing Crypto

Buying crypto is another type of transaction that the IRS will not tax. As the asset is being held and has yet to be sold, the investor does not have to report the crypto assets they have purchased.

Gifting Crypto

If one wishes to gift crypto to another person, the gifted amount cannot surpass the annual limit of $15,000. If the gift exceeded this yearly threshold, the excess amount would be added to the gifted person’s income and taxed accordingly. The IRS’s extended requirements regarding gifting crypto can be found here.

Transferring Crypto

Lastly, transferring crypto assets from one digital wallet to another cannot be taxed. If a person wishes to transfer their digital assets to another wallet, they must use a private key. A private key is used to transfer digital assets, and the secret number associated with the key is needed as it verifies the ownership of the account holder.

When to Report Cryptocurrency on your Tax Return

Now that the differences between taxable and non-taxable events have been determined, it is essential to know what to report on the tax return. Three primary transactions involve crypto: buying, selling, and earning crypto for a service. Depending on the activity involving crypto, it may or may not be disclosed on the tax return.

Purchasing Crypto

As mentioned before, when initially investing in cryptocurrency, the purchase amount does not have to be recorded, similar to when shares are bought on the stock market. They are not recorded because there are no gains or losses associated with this investment yet. Thus, the IRS does not require the initial purchase of cryptocurrencies on the tax return.

Selling Crypto

Selling any investments in crypto are required to be disclosed on the tax return. The IRS’s reasoning behind allowing the selling of crypto to be disclosed as income is due to the capital gains caused when selling these investments.

Capital gains are when an investment is sold for more than its cost. Consequently, the higher price it was sold at results in a profit for the investor, which is deemed as income under the IRS, and, therefore, must be disclosed.

However, there will be instances, especially with cryptocurrency, where investors will sell some investments at a loss. Consequently, the investor must also disclose the loss on the return, resulting in a tax credit, as a loss lowers the tax that one must pay on the net income. Fortunately, the IRS allows tax deductions up to $3,000 in relation to cryptocurrency transactions.

Image Credit: Shutterstock.com

Receiving Crypto for a Service

Lastly, it must also be recorded as income when receiving crypto for completing a service, such as a cryptocurrency exchange Coinbase’s Earn rewards program. For example, if a person receives 1 Ethereum for completing a service, they must recognize the Ethereum as income.

The value associated with Ethereum is the fair market value of the crypto asset when the recipient first received it. So, for example, if Ethereum’s value were $3,500 when the person received it, then on their tax return, their Ethereum income would be $3,500.

Furthermore, the same principles apply regarding crypto mining. Whatever amount of crypto mined would be regarded as income, and its value would be the market value when it was mined.

Tax Rates for Filing Crypto

When filing crypto, the tax rates vary depending on the filer's intention with their digital assets. For example, if the filer wishes to trade crypto throughout the year consistently, their income from crypto is viewed as short-term. On the other hand, if a person holds onto their digital assets for more than a year, it is considered to be a long-term investment. Depending on the investor's intention, they have different marginal tax rates.

Short Term

Concerning short-term investments and the constant trading of crypto, the IRS states the net gain or loss from these transactions can be taxed typically, using the typical tax rates.

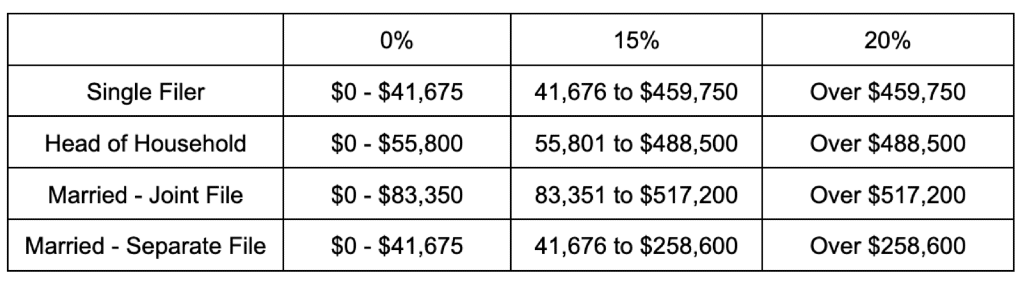

Long Term

When it comes to long-term investments, the process is different. The IRS has assigned different rates for those who have long-term crypto investments. Below is a table explaining the IRS’s different marginal rates for long-term capital gains, but the rates can also be viewed here.

Consequences of Failing to Report Crypto on Tax Returns

Although not wanting to report the gains made from crypto investments seems tempting as the tax bill will be lower if one has to pay additional taxes to the government, it is also difficult and illegal to partake in these actions. If the IRS’s tax system flags a return and triggers a manual review and suspicion of tax evasion, various detrimental consequences could follow.

Image Credit: Shutterstock.com

Criminal Charges

If the IRS suspects that a person is willfully falsifying their income to reduce their taxable income, the IRS will conduct a thorough investigation. If the IRS believes the person is willingly misleading them, they will charge them with tax evasion or tax fraud.

Severe consequences will follow if someone is found guilty of tax evasion or fraud. Firstly, the person will receive jail time, a sentence that will carry a maximum sentence of 5 years.

Hefty Fine

Furthermore, if the person becomes convicted of tax evasion or fraud, jail time is not their only problem. Typically, the IRS will also impose a fine of up to $100,000, which the offender must pay back, severely affecting their financial status.

Repayment of Taxes

The last and most detrimental consequence of tax evasion is the repayment of taxes. As the disclosed income was lower than it was, the tax amount paid was also less. Thus, the remainder that the offender did not pay due to the understated income must now be paid when a person is convicted.

This consequence is the worst of the three, as besides potentially spending years behind bars, the offender must pay back the amount of taxes remaining from their actual income. By paying back the remaining taxes due, this large debt causes the offender to most likely go into debt.

This is similar to the case of Jordan Belfort, the main character in the movie “Wolf of Wall Street." Although he did not have to pay back taxes, he had to pay $110 million back to the government due to his fraudulent actions.

Consequently, due to the large amount of money he has to repay to the government, he will most likely be in debt for the rest of his life, as his 2021 worth was negative $100 million.

Investing in cryptocurrency could potentially be beneficial as it could result in high profits quickly. However, due to the income gained from trading crypto, the taxes paid to the IRS reflect the correct amount of money earned. Therefore, it is essential to view Jordan Belfort as an example of what not to do as the penalties for tax evasion are severe, and it is not a wise decision to try and pay fewer taxes, as the IRS will catch on sooner or later.