Credit is King: How to Navigate the Debt Collections Process

- Knowing the process allows you to better understand how to handle debt collectors.

- Documentation is the key in the process of unlocking collections from credit reports.

- Planning SMART financial goals will allow you to negotiate better when it comes to your outstanding balances.

Even beyond the pandemic, the notion of "cash being queen" and "credit being king" has been stated and shared in real life along with on social media. But what happens when you get a letter in the mail or a missed call from an unknown number stating you owe them money?

If you receive a phone call from someone saying, "You owe me," like the Nas classic, it may mean that you've slipped up on a one-time payment or monthly payments. If that is the case, the missed bill has been placed into collections by a service provider or financial institution.

While a strong credit score and history are what we strive for, life happens. Although being sent to collections may hurt your credit score and temporarily impact the financial goals that you have for yourself and your future, you shouldn't allow such a hiccup to make you feel that things can't improve for your finances. They can, and they will.

Debt Collections Impact on Your Credit Score

A credit report is a statement that shows your credit activity, including your payment history of paying back a personal loan or when and with whom you have applied for credit. In addition, your credit report includes your credit score, representing your creditworthiness as a consumer and allowing creditors to see if you are responsible and trustworthy in paying back debt. A credit score can range from 300-850, with 300 being poor and 850 being excellent.

Recommended Read: What is a Credit Profile and How Can I Repair My Credit?

FICO and VantageScore are the two most popular credit-scoring models, but the credit score ranges and percentages weigh differently. However, regardless of looking at your VantageScore or FICO, late payments and collections will still impact your credit score and are considered a major factor. Regarding your FICO score, the more popular credit scoring model, late payments and collections make up 35% of your credit score. The rest of your FICO credit score is made up of payment history, amount owed, credit history, credit mix, and new credit.

Working Through The Debt Collection Process

Debt collection usually starts when a bill is overdue by 120 days or more, depending on the debt type. However, prior to a creditor possibly selling your debt to a collection agency, the original creditor will try to work with you to rectify the past due amount.

Because collections will impact your credit score, there are some steps to take that will allow you to make sure that your score stays stable and eventually soars. The process may be a pain for most, but it will pay off in a major way down the line by crushing the debt and gaining knowledge.

When you receive a notice that a creditor is attempting to collect a debt, what should you do next? First, it is important to note that you should never ignore a bill collector when they are trying to get in contact with you. Ignoring the debt doesn't make it magically go away or decrease the owed amount.

Recommended Read: 4 Credit Traps to Avoid

If a debt collector contacts you, there are two things that you must verify:

- Ask the collector to provide you with information about who they are and the origin of the debt in question. Due to scammers who often pose as legit debt collectors, be sure that you are not sharing personal information upfront, especially online, since debt collectors can now contact you via social media.

- Verify if the debt is valid. The surest way to do this is by sending them a debt validation letter. The validation letter will create a paper trail of your progress.

Debt Validation Letter

Within a debt validation letter, you have to reference the debt in question and ask the collection agency to provide actual proof of that agreement. Make sure you list the account information and payment amount they provided to you within the document.

Be sure that you receive a certified debt validation letter from the agency. The letter allows you to track the process, which is vital due to the time stipulations. The agency has 30 days from the date they receive the debt validation letter to submit proof to you that the debt is yours. You want to ensure that you keep a copy of the letter for your records.

Your next step will be dependent on the collection agency's response to your letter.

Option A: The Debt is Yours and Valid

If the collection agency submits a document to you proving that you owe them money, the next step is to make a plan of action before you contact them.

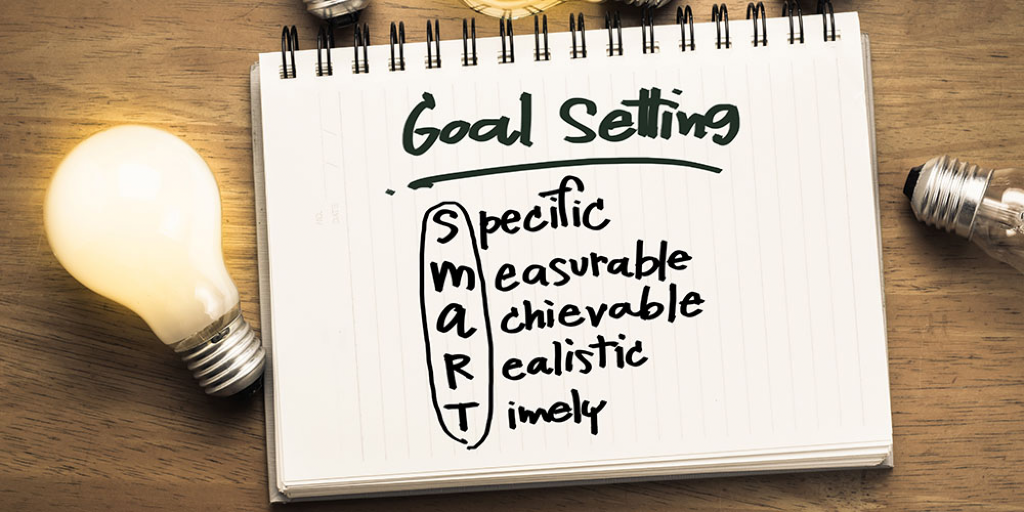

Create a SMART goal to guide you in the process of paying off your balances. The plan will allow you to negotiate if necessary. Next, contact the agency via mail or phone to arrange a payment plan or lump-sum payment for all or a portion of the debt. Collectors often get your debt for pennies on the dollar, so any amount that they get within range of the original amount is golden.

Whatever payment arrangement you make with the collection agency, be sure to get the agreement in writing and mailed to you. Having the agreement document will protect you in the long run, especially if a scammer tries to collect on the same debt.

After the debt is paid off, have the creditor submit the updated status to all three major credit bureaus–Experian, Equifax, and Transunion. It may take 30-90 days for your credit report to update to show that you paid the outstanding balances in full and start to restore credit.

Option B: The Debt Isn't Valid to be Collected

This option applies if the debt isn't yours, the collection agency never responded within the required 30-day timeframe after receiving your debt validation letter, or the debt is old. Although it varies by state and type, sometimes debt can be outside the statute of limitations and can no longer be collected. In this case, collectors can't collect or sue you over the balances they state that you owe.

If you find that the debt the collection agency is trying to contact you about is not valid to be collected, you need to write a letter to all three credit bureaus and request that the debt be removed from your credit report. Also, ask each for written confirmation when the debt has been removed.

Know Your Rights

Even if your debt goes into collections, you have rights. The Fair Debt Collection Practices Act (FDCPA) was designed to protect consumers from unfair and deceptive practices by debt collectors. The FDCPA mandates how often and when a collector can contact you, including outlawing their ability to contact you at work. Knowing your rights will help keep you safe during the collection process. Another great resource to know about your rights is The Consumer Financial Protection Bureau (CFPB), along with your State Attorney General.

The More You Know

The core of the process is documentation because it helps you keep track of getting the collections off your credit report. Your credit report and credit score are a form of your identity, rights, and wealth. Therefore, creating a habit of knowing the pulse of your credit is critical. As you continue to grow in what you know, you can grow within your financial journey.